One Deal, Three Quotes, Different Outcomes: How the Best-Looking Quote Could Cost You Thousands.

The same loan scenario can produce very different DSCR loan quotes depending on who's quoting it, so comparing quotes side by side isn’t always simple. Sometimes, the seemingly best deal isn't necessarily realistic. Here's how that can happen.

Meet John - a real estate investor in the South Carolina Lowcountry. John works full-time as a data engineer in corporate America and invests locally in long-term rentals and flips. John has acquired three rental properties by buying a new home every few years, converting the old homes into rentals. Now, John has leveled up: he’s bought and rehabbed a distressed duplex in Charleston County to add to his portfolio.

John purchased the duplex for $275,000 and spent nearly $50,000 renovating it over five months, financing the deal with a $250,000 fix-and-flip loan and his own cash. He’d completed the rehab and he owed $250,000 on the fix-and-flip loan, which was maturing in just over four weeks.

John’s plan was to get a $300,000 refinance loan; enough to pay off the fix-and-flip loan and get back some of his cash. He planned to rent each duplex unit for roughly $1,700/month, had ballpark numbers for expenses, and figured the property was worth around $400,000.

The major focus for John was moving quickly on a DSCR ref. He would owe a $7,500 extension fee on the fix-and-flip loan if it was not paid in full by the maturity. John couldn’t stretch the timeline - he needed to close on time to avoid the extension fee, and he didn’t want a Conventional loan because he knew his DTI would be too high. Still, he felt that he could get a couple loan quotes from competing lenders quickly enough to get a good rate.

So, John did what many investors think they should do: he got a few loan quotes to shop for the best rate.

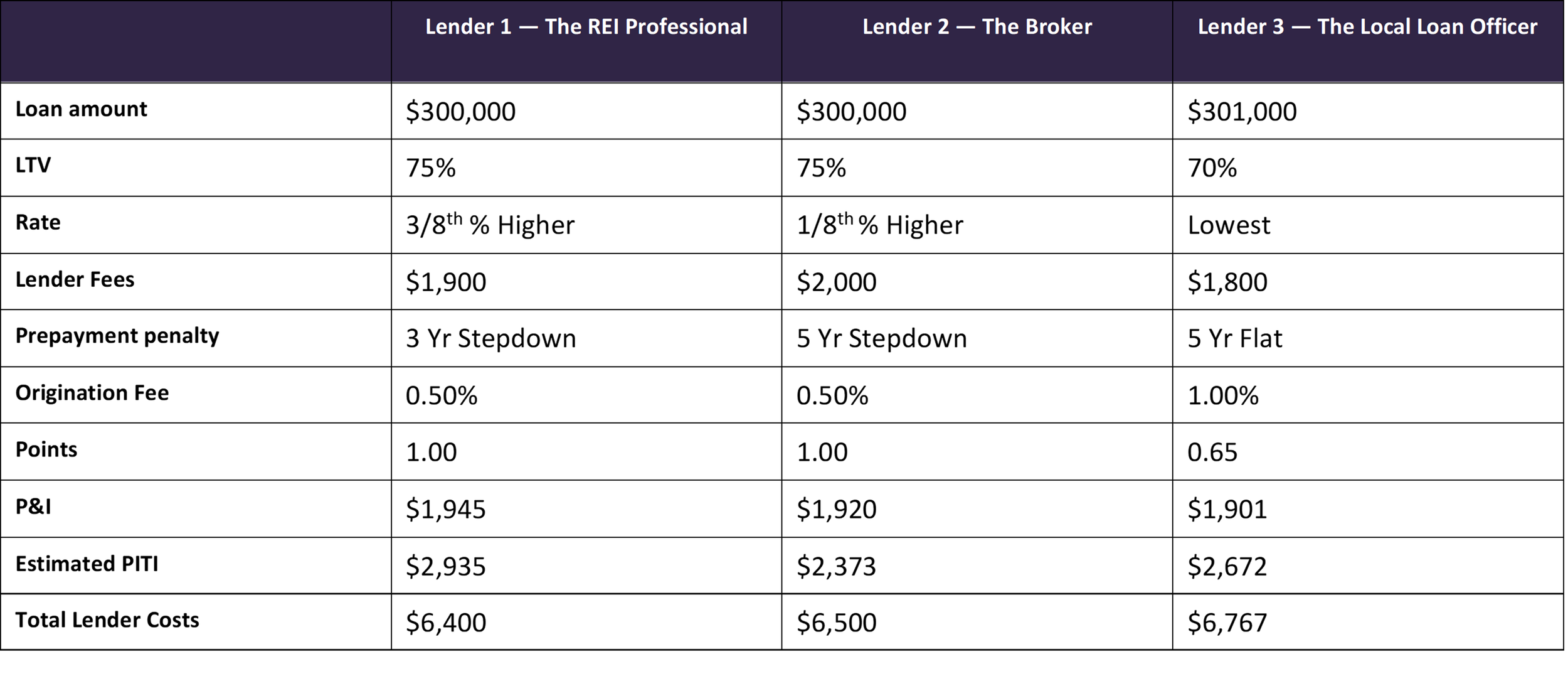

The Three Quotes

John called three lenders, completing an application and getting a quote from each. Side by side, the Professional’s quote looked the worst - a higher rate and a major difference in the monthly PITI payment. The Broker's quote looked noticeably better, and the Loan Officer's quote looked like the best of the three. John based his decision on the numbers in front of him, which seemed like a no-brainer.

This seemingly straightforward method got John into a mess that cost him thousands. Here's how.

Table showing the terms of each quote.

John called three lenders, completing an application and getting a quote from each. Side by side, the Professional’s quote looked the worst - a higher rate and a major difference in the monthly PITI payment. The Broker's quote looked noticeably better, and the Loan Officer's quote looked like the best of the three. John based his decision on the numbers in front of him, which seemed like a no-brainer.

This seemingly straightforward method got John into a mess that cost him thousands. Here's how.

Lender 1: The Professional REI Lender

John’s first call was to a lender who worked almost exclusively with real estate investors in only a few markets, including South Carolina. The Professional had several years of experience, had a formal lending background, was fully licensed, and was an investor himself. He asked John detailed questions – not just about the property, but also about John’s plans for this particular property and his portfolio in general, as well as what John wanted to achieve with the refi.

John explained that he wanted to recover what cash he could, but that he really needed to close the refi asap to avoid having to pay the extension fee on his current loan. His long-term goal was to balance cash flow with leverage; he planned to pay down the principal with any extra cashflow over the next few years to around 65% LTV and then refi into a lower rate when he could. He wanted to balance getting a good rate with low costs and flexibility – he didn’t want to be trapped in case rates dropped.

The Professional went through a detailed pre-underwriting process, which included price and rent comps for the property, checking the flood zone and history, and estimating taxes. The property sat in a flood zone, which is common in the Lowcountry and meant flood insurance costs needed to be accounted for. Taxes were calculated using the County’s actual non-owner-occupied assessment ratio and millage, as the prior year's owner-occupied tax bill could be 3X too low.

The Professional called John back with the quote, detailing how it reflected conservative and realistic outcomes for his scenario. He walked through how the figures for rent, appraisal value, insurance/flood premiums, and taxes were estimated. He showed John the trade-offs and costs between the different prepayment penalties, explaining that John could get a lower rate or points by choosing a more restrictive prepayment option at the cost of being able to refinance when he wanted to. The Professional helped John weight the trade-offs, and John decided on the 3 Yr Stepdown prepayment as the best balance for his goals.

The figures the Professional used for the quote:

Est. Value: $400,000

Est. Rent/Unit: $1,700

Est. Annual Hazard Insurance: $3,500

Est. Annual Flood Insurance: $1,400

Est. Annual Property Taxes: $7,000

DSC Ratio: 1.14x

LTV: 75%

Lender 2: The Nationwide Broker

John’s second call went to a loan broker who'd been chatting with him on social media. John had been asking questions about DSCR rates in an investor forum when the Broker commented that John would “definitely be low 6’s” and that he was “happy to jump on a call.”

The Broker operated virtually, working deals across 36 states from home. On the surface, he seemed legitimate, including a sharp website with 5-star reviews. This wasn’t quite the case, though.

What John didn’t know was that this Broker had been working as a lender part-time for less than a year, and his only training was a course he’d bought from an ad on YouTube. The Broker was not NMLS licensed, since business-purpose lending doesn’t require licensure either nationally or in South Carolina.

While being licensed is far from a guarantee of competence, the flip side is that anyone without a license (or expertise) can call themselves a broker, lender, or loan consultant and offer business-purpose loans. Some unlicensed lenders are skilled, reliable, and experienced. Some are well-intentioned but in over their heads. The Broker fell into the second category.

The Broker used John’s rough figures - the same ballpark valuation and expense numbers John had given every lender. He grabbed last year's tax amount, not knowing about South Carolina's non-owner-occupied rate. He used a generic national average for insurance that didn’t include coastal South Carolina storm risk pricing. He never even thought about flood zones, which, on a Lowcountry property, can significantly affect the costs.

The Professional had checked and updated these. The Broker didn't.

Even more damaging, though, was this: the Broker quoted his best loan program simply because it had the best terms - without fully understanding it. Not coincidentally, this program was also the strictest, including requiring six months of ownership (which John didn’t have) before any new appraisal value could be used in the refinance.

None of this was malicious. The Broker was simply inexperienced and incompetent.

The figures the Broker used for the quote:

Est. Value: $400,000

Est. Rent/Unit: $1,700

Est. Annual Hazard Insurance: $2,500

Est. Annual Flood Insurance: $0

Est. Annual Property Taxes: $2,919

DSC Ratio: 1.43x

LTV: 75%

Lender 3: The Local Loan Officer

The third call went to a loan officer with over two decades in the business - mostly Conventional and FHA/VA lending - with enough DSCR experience to be credible. He was recommended by John’s realtor, and he was polished, confident, and had hundreds of good reviews.

He was also an experienced salesman who knew exactly what he was doing.

When he talked to John, he didn't ask the questions the Professional had asked. Instead, he made it all about the rate. He nudged every assumption toward best case scenario. He spun every variable to his own benefit.

The appraisal would “almost certainly” come in higher than $400,000, he said - Charleston's market was hot, so he assumed a higher estimated value. He asserted that the rent would be at least $1,850/month because Zillow said so. When it came to insurance, he assumed a best-case premium, the kind that was possible, but likely.

Run through those generous assumptions, the loan looked excellent - DSCR comfortably above 1.25x and LTV at 70%. This was the basis for the Loan Officer’s quote; it was technically accurate to the inputs, but highly unrealistic.

Disclosed in the documents but never fully explained was a five-year flat prepayment penalty. The Loan Officer didn’t bring it up until John, not understanding how it worked, asked about it. Being well-versed in old-school sales spin, the Loan Officer handwaved away John’s concerns, saying “You don’t plan to sell it in the next 5 years, right? Then you don’t need to worry about it” and claiming the “major improvement in the rate” made it worthwhile.

The Loan Officer pointed out that the Broker’s tax quote was too low and didn’t account for flood insurance, correctly asserting that these would increase. He also compared his quote to the Professional’s, saying that his fees were lower and that the savings at the lower rate was over $16,000 (implicitly meaning over thirty years).

The Loan Officer wasn’t doing anything illegal – he was using technically accurate information but was spinning it in a way that created a misleading perception. His aim wasn’t to provide John with reliable guidance; it was to win the deal and earn a commission.

The figures the Loan Officer used for the quote:

Est. Value: $430,000

Est. Rent/Unit: $1,850

Est. Annual Hazard Insurance: $2,400

Est. Annual Flood Insurance: $850

Est. Annual Property Taxes: $6,000

DSC Ratio: 1.39x

LTV: 70%

What Happened Next

John went with the Loan Officer. The numbers were the best he'd seen, the guy had two decades of experience, and the Loan Officer made it seem like nothing could go wrong.

The appraisal came back at $402,000 and the rent schedule at $1,675/unit - within expectations, but short of the optimistic numbers the Loan Officer had quoted. The insurance costs, once real policies were obtained, landed well above what both the Broker and the Loan Officer accounted for.

Underwriting updated the loan using the real figures, which pushed the DSCR well below 1.25x and LTV up past the 70% that had been quoted. The rate increased – a lot. So did the points.

When John got the changes, he pushed back. The Loan Officer made excuses - “the appraisal came in low – the appraiser’s an idiot” - as if the gap between his quote and reality had been bad luck rather than manipulation. After the changes raised suspicions, John asked direct questions about the five-year prepayment penalty. To his frustration, he learned that if he refinanced or sold within the first five years, he would owe a 5% penalty - meaning five points on the prepaid amount. If he lowered the prepayment period, it would add another point to the costs.

By then, John was 10 days from his deadline. Switching lenders meant restarting from scratch – a nearly impossible timeline. He closed with the Loan Officer with terms meaningfully worse than the original quote, and worse than the Professional’s quote had been from the start.

The final numbers:

Value: $402,000

Rent/Unit: $1,675

Annual Hazard Insurance: $3,328

Annual Flood Insurance: $1,317

Annual Property Taxes: $6,978

LTV: 74.6%

Final Points: 1.85

Final P&I: $1,970

Final PITI: $2,940

DSC Ratio: 1.14x

Final Lender Costs: $10,350

How This Happens

The pattern here isn't unusual. It's close to routine in DSCR loans for two very different reasons: incompetence and misleading sales tactics. In the end, though, they produce the same result: loan offers that aren’t attainable.

Had John worked with the Broker, the loan program would have changed entirely once Underwriting scrubbed the file. The damage was fatal; John hadn’t yet owned the duplex for six months, so the LTV would’ve been based on $325,000 (the purchase price plus rehab costs) – not the appraisal amount. This flaw had been baked into the file from day one and had nothing to do with the actual appraisal or estimates. This loan quote wasn’t just a little off – it was wholly out of reach, which would’ve resulted in worse terms or possibly even outright denial.

The Loan Officer's quote changed because he’d built it on assumptions he knew were unrealistically optimistic. He’d been using this “tactic” for years; it was a variation of the classic bait-and-switch. He created a picture-perfect quote that beat the competition to lock John in, knowing it would be too late to switch lenders once the terms changed. He then blamed everything else - the appraiser, the market, bad comps, etc – to save face.

A DSCR loan quote is only as good as the assumptions behind it – and this can create huge discrepancies between offers. Rate is the easiest number to compare, but it’s also the easiest number to manipulate. The final terms of a DSCR loan are driven by the actual figures, not the estimates used in a quote. Experienced lenders know this, and it’s part of what separates the sales reps from the professionals. Sales reps use this knowledge to “win deals” and sell loans. Professionals use it to guide you in making decisions about your financing.

A few questions could’ve changed the outcome for John if he had asked them before picking a lender:

· Is there a prepayment penalty, and if so, walk me through exactly what happens if I sell, refinance, or pay off the loan early?

· Could this quote change for any reason, like if estimates are off? What’s a reasonable worst-case quote look like?

· If the terms can change, when would this likely happen? Are there fees or costs I’d lose if I walked away?

· If you had to make any judgment calls in setting up my loan, could you walk me through what they were and how you made them?

Rates and fees matter, but getting the best deal on an investment property loan isn’t as straightforward as just comparing loan quotes. An incompetent or misleading lender can cost you thousands of dollars - or even your deal. Skill, expertise, and honesty play into the value a lender brings to your loan. Make sure these are part of your calculus when choosing a lender to work with.